Kristina Manjula

What attractive Peer-to-Peer loans for investors

The P2P loan market, that is, loans from individuals to individuals with the help of online platforms without the participation of banks, resolutely increasing volumes: new services appear, the players have received large investments. Many media, not taking place in expressions, call the propagating services of P2P lending "killers of banks". So what is P2P lending? RusBase has already answered this question in the Oktyabrsky review. Today, we will carefully consider this market, in particular, Russian P2P startups, as well as online lending services close to MFIs.

P2P lending, person-to-person lending, peer-to-peer investing, "peer-to-man lending", "Man lending to man", "Social lending" is a direct issuance of loans from the contributor to the borrower without the participation of traditional financial institutions, There are banks. This service provides Internet services, where the user can act as an creditor and the role of the borrower. Summary natural exchange of money: one puts, the other takes. The cheapness of the online site, unlike the expensive mediation of the bank, theoretically allows such services to do low bets on the consumer creditAnd the investor is to increase the income from the deposit. If the service takes a modest 1-2% commission, the loan is issued under 20% and less commission, the lender receives its 19% instead of 10% of the contribution, and the borrower loan costs 21% per annum. However, in practice, it sometimes looks different, especially in the Russian market.

Of course, the new type of lending is still with some caution, and it is no coincidence. Security of deposits ensure the services themselves, trying to get the maximum customer information, but the loopholes remain, and legal system does not control this species financial relations. P2P companies trust their money or not, it is worth judging by looking at the experience of other depositors, as well as on the growing volumes of the market. According to the UK Peer to Peer Finance Association, at the end of 2013, 3.7 thousand P2P businessmen borrowers and 70 thousand borrowers took a loan on consumer needs. They accounted for more than 86 thousand active lenders. In general, over the past year, the global market volume grew by 121%.

The first such service appeared in the UK in 2005 under the ambiguous Zone of Possible Agreement for the Russian ear. Zopa and now remains the largest peer in the country with a base above 500 thousand customers and the volume of loans issued more than 469 million pounds. A year later, two more serious players appeared in the US P2P lending market: Prosper and Lending Club. By 2014, quite a few similar projects spread in the world and many of them begin to attract large finances from famous investors. For example, Prosper in 2011 received a total of $ 95 million investments, including money from the Eric Schmidt Foundation, Chairman of the Board of Directors of Google. And in the largest Lending Club service, an estimated at $ 2.3 billion, an estimated $ 57 million owner Mail.Ru Group Yury Milner. Among the popular foreign P2P companies also international Kiva, CommunityLend.com (Canada), SMAVA.De (Germany). In the United States, there was even a startup, uniting two revolutionary trends in the economy, such as bitcoins and peer-to-peer lending: Cryptomets can be obtained via the BTCJAM platform.

Russian market P2P lending

To Russia, P2P-Online credit services reached Russia only in 2010, and they began to actively function only in 2012. The market itself is presented for the most part of the microloan system. In the review, we took into account the companies that act on the classic Peer-to-Peer system, that is, they accept deposits from the population and projects close to MFIs based on trust and exercising lending online, but for money funds or professional investors.

One and the oldest companies - "Svddzh.ru" . The service allows you to take a loan without references and guarantors online. Borrower fills on the site credit formThe administration verifies information and assigns the client from 1 to 100. If the client provides credit history, it will significantly increase creditors' rating and trust. The obligation the borrower takes the same as in the bank, concluding a loan agreement: the relationship after is regulated by the relevant legal instrumentaries. Loans from 2 thousand to 100 thousand rubles, on average sums of approximately 5 thousand rubles are issued. Accordingly, the interest rate for the borrower is calculated by the administration depending on the credit history of the client. On average, it is 25%, according to the company's general director, Anton Tarasov. As for interest interests, the effective indicator is 30%. The minimum investment is 4 thousand rubles recommended to reduce damages - from 40 thousand. The site has a calculated table for depositors.

Anton Tarasov, general director of the company "Svtzh.ru":

Anton Tarasov, general director of the company "Svtzh.ru":

As a source for financial investmentsOur tool rather competes with others, but complements them. It is located in the risk zone and profitability, in which there are no other competitors. If we take Forex, then this is a huge risk and, perhaps, good yield, but at the same time it is few people manage. Another extreme is banks: one hundred percent yield, but low interest. If you look at the market above and take stocks, where there is a big yield than in banks, less risk than Forex, but the likelihood of a complete loss of money. For stock, you need high professionalism from the investor to understand what to do when quotes go down. It is easier to a little with bonds, but the yield is not much higher than on deposits in the bank. So we are in the middle. Our tool is clear. It is clear who it is and what it is, where they are investing and where, in general, money. You can trust and can be investing: For investors, we advise you to diversify a portfolio in different directions, including our tool, as complementary.

Similar system "Credit Exchange" WebMoney system also has been successfully operating for several years and is recognized as experts. To get a loan, you must have an electronic wallet connected to the TRANSFER system. You specify what amount, for what time and under what interest is ready to provide a loan, and the system selects suitable suggestions. Accordingly, the proposals form also users: if you have any free amount, here you yourself can give consumer credit. The loan rate is an average of 25%. In the entire history of the work, more than 91 thousand loans were issued for a total of almost $ 30 million. Security of deposits is guaranteed by special certification of users, but experts advise to check their borrowers and independently, although the loan agreement is also issued, which is a guarantee for litigation.

According to the similar principle, the Site "Bangka" works. The top offers of creditors and borrowers are ranked on the main page, the user is registered by checking the service and receives a rating. 21 thousand users were registered in the Babank system, 17 thousand transactions were concluded in the amount of about 140 thousand rubles.

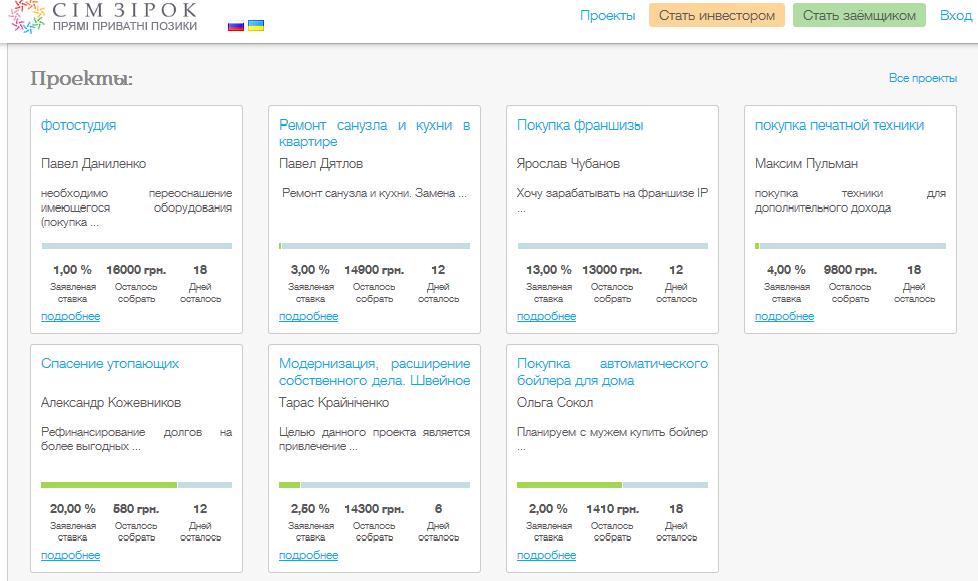

Another special view Microloan services is a sort of "breakfasting", only without a venture component. This, for example, the Loanberry service, which acts on the same P2P "scenario", where lenders are found with borrowers, but it is indicated here that it is taken or is given off (repair of an apartment, for example). Lenders can form part of the amount - fees are obtained, as on trumpplatforms. There is a similar service in Ukraine - this is a startup simzirok. The project is still the only one in its kind on the Ukrainian market, he started recently, received investments from Imperius Group (RVK). Its feature is forced diversification, that is, the limitation of the maximum amount of investment in one loan one creditor and a completely unique auction method for establishing interest rate. Here, users declare about their projects, and, for example, about the desire to "buy an automatic boiler with her husband."

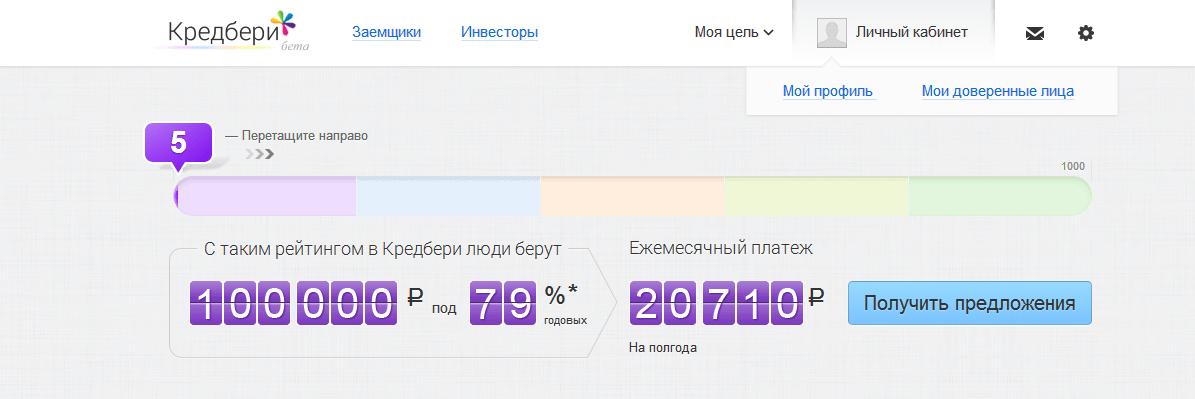

Last month, a new player was released on the P2P market - the project Credberry.ru, who launched Maxim Nogotkov, owner of the company "Svyaznoy". The project generated the experience of its competitors and came up with a combined mechanism: loans to each other, calculation of rated rates, calculation of credit history rating, guarantor friends and user reviews of borrowers. First, Credberry is looking for applications for banks, among which "Svyaznoy. Bank" and "Renessance Credit". Secondly, a private investor can be found through this platform. The service calls its services to "trust lending." The ranking takes into account the volume of data, profiles in social networks, feedback from friends, users. In addition, you are passing specially designed tests on banks. The service is still available in beta.

There are also a number of companies on the periphery of P2P lending, because they are not contributing the contributions of the population, but money of professional investors and funds. They are closer to microfinance organizations, but also draw up loans online. Interest rates here are colossal, but such types of loans are designed for those who need to get small money urgently on short term. For example, if you need to urgently give a rent for an apartment, and the neighbor has to ask for a debt! In addition, such services are interesting for large investments, since very profitable.

The MoneyMan platform was founded in 2011 by Boris Batin and Alexander Dunaev, in 2012, the service began its work, and in 2013 the owners announced the closure of Series A funding in the amount of $ 3 million. Last year investments received investments from Vadim Smymov (smoke products , chain of stores "Republic"). According to Boris Batina, this is "the first service in Russia, which is automated processes applications and issues loans in full online." The service issues urgent loans up to 15 thousand rubles. Registration in 5 minutes, money on the same day, without leaving home. Although there is a network negative feedbackWhat are the delays and some other errors. However, the customer service is really convenient for the client: on the site there is a very clear loan calculator, as well as a smart marketing system bonus points For the timely repayment of the loan, which can be further used to extend the loan period, reducing the interest rate or increase the amount of up to 30 thousand rubles. True, interest is extremely high: if you take 8000 rubles, let's say, for a month, you will have to overpay more than half. And this, if you estimate on the calculator, and relate to long-term credit In a bank or through P2P ... Attention: 744% per annum! The Commission, of course, is colossal, but this is a fee for urgency and relative non-interference in a credit history.

Similar services - Milli and Cashier 365. Milli is a very ambitious startup collaborating with Euroset. You can get a loan to 30 thousand, having only a profile in one of social networksAfter arriving in one of the mobile retailer salons on the Corn Map. "Cassas 365" issues from 2 thousand rubles. up to 15 thousand rubles for 5-15 days.

Experts on the prospects and problems of the P2P lending market

Anton Tarasov, general director of the company "Svtg.ru":

The main problem is the imperfection of our banking legislation. The mechanism for the conclusion of loans is similar to both in Russia and in England and the United States, but in the issue of the interaction of the lender and the borrower, in the form of money transfer, we will be sent relative to developed countries. In the same England there is, for example, accounts trust management. They have a much larger aspect of use than in Russia. In Russia, this is the management securitiesAnd there it can be anything - and material things, and brokerage. It simplifies the calculation system itself. In all the rest, we are no worse, no better. Only in the west of money more in terms of creditors' fundation. There are simply physically creditors. People are simply not yet accustomed to the fact that there is an alternative to banks that you can earn somewhere except in a bank, and some minimal risk suffer.

Boris Batin, the co-founder of the Moneyman project:

Boris Batin, the co-founder of the Moneyman project:

Of course, the business created on the P2P principle is interesting, and, as the international analogs show, is very profitable (for example, Zopa.com). But it must be borne in mind that, despite the similarity of the final product (loan), P2P and B2C are 2 fundamentally different business. In the case of microfinance organizations, as ours, the earnings go through a qualitative assessment of the borrower. P2P is a platform business based on commission with the involvement of 2 parties. MFIs have more risks, as the funding comes from its own budget, but potentially more profitable. P2P projects require more time to develop, potential earnings below, but also the risks below. As for problems, companies based on the P2P platform are faced with the same faced by any new business - It is distrust of the consumer. In fact, a person giving a loan must trust the platform or broker when evaluating potential borrower. And in Russia, unfortunately, few people can competently assess risks when issuing a loan. There are also a number legal problems (for example, laws on credit stories) that make it difficult to work P2P services.

Vyacheslav Artamonov, Head of SIMZirok:

Vyacheslav Artamonov, Head of SIMZirok:

Market problems can be listed for a long time. Absence effective system Banking cashless payments (direct write-off and reservation) and electronic banking. Insufficient development (functionality) and efficiency of electronic money systems. Lack of legislation and practices using Escrow Accounts (Segregated Accounts). Barrganizing payment rates visa systems And MasterCard. Skeptical sentiment of investors / lenders. Insufficient (albeit high) Internet penetration. The lack of a clear scheme for identifying customers online, which is characteristic not only for the markets of Russia and Ukraine. Difficulties of obtaining data on clients from electronic databases, including the Bureau credit stories. There is no sufficient practice of consideration of such affairs in the courts. Lack of a clear concept "clean interest income"(Deducting non-returning debts from the amount of income). The lack of a clear mechanism for collective decision-making by the leiners (there is no concept of "syndicated loan" - analogue "Syndicated loan"). Lack of a clear gear mechanism (sale) debt collector agencies.

Dmitry Alimov, Managing Partner Frontier Ventures:

Dmitry Alimov, Managing Partner Frontier Ventures:

P2P projects investment are attractive, as they constitute competition to banking services. With the right organization of business, their costs are lower, which gives them a competitive advantage over traditional borrowing and accumulation tools (first of all, banking products). There are not enough high-quality projects in all segments, but their shortage in the small business P2P lending segment is especially noticeable.

Found a typo? Highlight the text and press Ctrl + Enter

Comments

- The first service of P2P lending was the British company with an indecent name Zopa. Since its inception (2005), private service investors issued loans in the amount of more than 500 million euros!

- Three types of P2P lending are distinguished:

- Consumer (for repair at home, payment of leave / wedding or refinancing loans)

- Small and medium businesses (unsecured loans or property provided by the company). Such loans are usually used to buy assets or development.

- Real Estate (for purchase commercial real estate or housing) - Loans at P2P lending are crushed into small pieces (from $ 25). Such a nuance reduces the risks of the lender. After all, in case of no return of individual microloans, the quality of the general portfolio will not seriously suffer

- Every month, millions of dollars pass through P2P platforms. It is expected that by 2016, the volume of the "man to man" loan market in the UK will be 5 billion euros, $ 30 billion in the United States, and around the world will overcome a plank of $ 60 billion

- Credits via P2P cost cheaper than credit card debt service

- In general, investing in P2P services less risky than investments in the stock market. This confirms the experience of 2008. At the beginning of the financial crisis stock market US asked 53%, and the P2P lending sector lost only 3%

- Most of the profit brought loans to refinancing debt and loans to the organization of weddings, moving and ... vacations

- Secured by vehicle

- On business development

- Purchase, modernization or repair of equipment, real estate or auto

- Refinancing loans (one or more)

- Redemption share in business

- In consumer P2P lending to individuals, small unsecured loans are issued. As a rule, it is used to finance large shopping, weddings, vacations, repair of the house, or to consolidate debts.

- When lending to small and medium-sized businesses, the loan is issued by the company and may be unsecured or secured by the Company's property, or by personal guarantees of the director or shareholders of the company. This kind of loans is most often used to finance the company's growth or purchase of assets.

- When lending to real estate used by private individuals and organizations for buying housing and commercial real estate, the loan was provided by the first stage of property pledge.

Dorris 12:53, 04/04/2014

FROITE 14:45, 11/20/2014

Evgeny Podstubin 10:45, 12.12.2014

Evgeny Podstubin Ruslan Ayupov 18:05, 12/13/2014

Evgeny Podstubin Vitaly 09:56, 05/13/2015

Natalia Istomnia 23:05, 22.05.2015

Raushan 13:08, 06/19/2015

Maxim 20:00, 9/11/2015

Semen 20:44, 01/13/2016

Nikolai Kudryavtsev 19:13, 18.01.2016

Kirill Ershov 15:07, 01/28/2016

Perry White 23:11, 04/22/2016

Ihende Abraham 22:52, 04/30/2016

Mark Vidal 22:51, 7.05.2016

Alberto Blackwell 08:07, 05/20/2016

Alberto Blackwell Mark Vidal 14:55, 06/09/2016

Alberto Blackwell Murat Ozapov 22:14, 01/24/2019

Davis Morgan 23:08, 05/26/2016

Skyfinancialoan Funding 09:18, 4.06.2016

Helen Anderson 06:20, 06/09/2016

Kate Alexandra 16:06, 11.06.2016

Timmons Brent 11:48, 06/16/2016

Timmons Brent 11:50, 06/16/2016

Mrs Zonat 22:44, 06/29/2016

Absolon Casimir 15:06, 7.07.2016

George Winston 15:02, 9.08.2016

George Winston 21:57, 9.08.2016

Mr Titcomb Brown 08:07, 08/20/2016

Annia Vicky 15:01, 08/28/2016

George Winston 05:40, 09.09.2016

George Winston 05:42, 09.09.2016

Michael Cedric 20:10, 09.09.2016

George Winston 22:03, 2.09.2016

George Winston 22:10, 2.09.2016

Nokumkz 06:02, 09.09.2016

George Winston 02:12, 09/12/2016

George Winston 02:15, 09/12/2016

Helen Anderson 06:04, 09/12/2016

Helen Anderson 06:04, 09/12/2016

Helen Anderson 06:04, 09/12/2016

Helen Anderson 06:05, 09/12/2016

And if seriously - today we can find a lot of ways to invest money under high percentageswithout risking to lose the whole amount in one minute.

And today in the center of our attention - P2P lending from the point of view of the investor.

P2P lending is when a particular Petya credits Vasya directly with his money. Expression " peer-to-peer"From English translates as" to each other. "

Borrowers receive borrowed funds under little percentagethan in a bank or MFI. And investors' lenders earn more loans much more than on deposits and others.

In general, R2P lending is a very interesting option for the borrower, and for the investor!

Internet Playground Loans "City of Money"

"The city of money" is the largest Russian Internet playground in the P2P segment, on which borrowers and investors are found.

Joint Stock Company is part of the General Invest Holding (Financial and investment activities). The Internet portal unites several companies in Russia, Luxembourg, Italy, Switzerland and Belarus (the project is not presented in Ukraine).

Important! As borrowers are attracted only commercial organizations and entrepreneurs. In other words, a loan for vacation in Egypt or to get here.

Loans in the "city of money" are divided into three types:

Borrowed funds on the site can be obtained on:

As collaboration, the liquid property of the borrower (equipment, special equipment, real estate, vehicles or the guarantee of third parties) is considered. All projects for obtaining loans come into open access only after a thorough estimate using the EBRIR technology. Service experts personally appreciate the business, leaving his reference.

First of all, the profitability and stability of the business, as well as the level of security and return loans are analyzed. The loan agreement lies between the borrower and the investor directly. The project participants can freely communicate with each other on the site and even conduct bidding at rates.

In the role of an investor can speak anyone: both physical and legal entity.

The minimum amount of investment from one lender is 10,000 rubles, and restrictions on maximum amount No at all. At the same time, the project can be financed either completely or partially.

As soon as the borrower's application collects the desired amount email Investors will receive a notice of the end of the trading with detailed loan conditions and the form of payment of the Commission "City of Money".

After paying the site's commission ( bank card or translating through the bank) A loan agreement and security is signed in the office of the "City of Money" (there is a borrower and a service representative).

A pair of numbers

At the end of November 2015, almost 10.5 thousand borrowers were registered in the service, and investors are more than 4 thousand. During all the time of operation, the site was approved by loans in the amount of more than 522 billion rubles!

Interest rates on loans in the "city of money" range in the range from 25% to 100% per annum. Additionally, direct investors pay 1% commission service. The playground works around the clock in 24/7/365.

My opinion: "Money City" - one of the most reliable services in this segment. In any case, it can definitely be considered from the point of view. Yes, and reviews about this platform on the network, for the most part, decent.

In my opinion, the platform is advantageously distinguished by a decent potential yield in combination with an acceptable risk level. Especially on the background of infinitely loved ones on the Internet PAMM accounts and Haipov.

And how do you feel about P2P lending niche? And specifically, to the service "City of Money"? Subscribe to updates and share the most interesting posts with friends in social networks!

1. P.2 P.-Credit as a service has existed since 2005. The first on the market was the British company Zopa, during its existence issued loans for £ 500 million and is currently being the largest player At the British P2P lending market with more than 500 thousand clients.

2. P.2 P.-Credit is not crowdfunding. In classic crowdfunding, individual investors are combined and finance a company that owns property in exchange for a share in it. With P2P lending, lenders finance directly individual, owner. When crowdfunding, the investor receives an increase in capital, and with P2P lending - income, and risk level at P2P lending are lower than in classic crowdfunding.

3. Mix three typesp.2 p.- Credit - consumer, lending to small and medium businesses, lending to real estate.

4. Loans at P2P lending are divided into small parts. This allows creditors to reduce the degree of risk by financing many small loans from $ 25, and if any of them are not returned, it will not be able to reflect a little on the quality of the portfolio.

5. The most reliable way to secure the loan whenp.2 p.-Credit is the key to the first stage for property. With this loan protection form, property in pledge can be sold to cover debt, and the P2P-loan is the first thing that will be covered after the sale of collateral.

6. Monthly throughp.2 p.-Thelatform pass millions of dollars. It is planned that by 2016 the volume of the P2P lending market will amount to £ 5 billion in the UK, up to $ 30 billion in the United States and up to $ 60 billion around the world.

7. Credits throughp.2 p.- Vlapporm on average cheaper than on credit card. This shows the practice of Lending Club, the largest P2P lending operator in the United States. If you compare $ 10,000 loans, taken through Lending Club under 12.4% and through credit card Under 18.5%, for five years, the credit on the map will have to pay $ 3050 more. It is not surprising that the overwhelming majority of P2P loans are issued to restructuring banking debts.

8. Investing B.p.2 p.-Thelatform may be less risky than investing in the stock market. During the financial crisis in 2008, the US stock market fell by 53%. Investors in P2P lending for the same period lost about 3% (Lending Club statistics).

9. It is more profitable to give credits for vacation than on training. Profit maximization requires a P2P investor to select funded loans in more than 30 different criteria. On average, the larger contributes to refinancing the debt (8.5%), the loans for the organization of weddings (8%) are led to them, for relocation (4.2%) and vacation (3.8%). Loans for training bring investors less than percent yield.

10. Loans with a good benefit ratio are funded for thirty seconds. New loans are available to investors several times a day, but among investors are so high competition for profitable loans that the latter are almost instantly financed. It makes the work of the P2P investor in something similar to the high-frequency trading - you need to have time to intercept profitable proposition before others.

Estimate:

15 0