Within the framework of this article, the main cases of the occurrence of the exchange rate difference will be sanctified, as well as how to reflect the exchange rate difference in 1C 8.3.

According to clause 4 of PBU 3/2006, the value of assets and liabilities in foreign currency or c.u. for display in accounting and reporting is converted into rubles. The difference in the assessment that arose as a result of this is called the exchange rate.

According to clause 5 of PBU 3/2006, the conversion is carried out at the official exchange rate against the ruble, i.e. at the rate of the Central Bank of the Russian Federation or at another possible rate, if such a rate is established by agreement of the parties. Another rate by agreement of the parties may be, for example, the USD + 1% rate.

The funds are recalculated (in the bank, at the cash desk), as well as the cost of "accounts receivable" and "creditors" * in foreign currency, which is carried out according to such rules as:

- By the date of receipt or write-off of DC in foreign currency / repayment of obligations;

- By the reporting date, i.e. on the last day of the month.

* Advances issued and received in this structure are not subject to revaluation.

The difference resulting from the recalculation will be reflected in accounting as other income or expenses (due to the fact that it is negative or positive) on 91 accounts. In the tax (income tax) it is reflected as non-operating income or expense on the same account, and it will not be reflected in the STS.

Set up the accounting of exchange rate differences in 1C 8.3

To set up exchange rate differences in 1C 8.3, first of all, you need to correctly set the details of the contract with the counterparty. In this case, we are talking about contracts denominated in foreign currency.

In 1C: Accounting 8.3, an agreement with a counterparty can be found at the "Contracts" link of the "Contractors" directory element or in the "Contracts" directory. Both guides are located in the "Guides - Purchases and Sales" section.

Figure 1 - Section "Contracts" of the element of the directory "Contractors"

Figure 2 - Directory "Contracts"

Consider two cases of concluding contracts in foreign currency.

If it is concluded with a resident, settlements can be made only in rubles, since in accordance with the Law of 10.12.2003 No. 173-FZ "On foreign exchange regulation and control" foreign exchange transactions between residents are prohibited.

In the 1C 8.3 program, the setting of a contract with a resident expressed in currency will look like this. In the section "Calculations" for the variable "Price in" the currency value will be set and the switch "Pay in" rubles will matter.

Figure 3 - Settings of an agreement with a resident

An agreement with a non-resident implies the possibility of mutual settlements in foreign currency, since in accordance with the Law of 10.12.2003 No. 173-FZ non-cash foreign exchange transactions between a resident and a non-resident can be carried out without restrictions.

In the 1C 8.3 program, the setting of a contract with a non-resident expressed in currency will look like this. In the section "Calculations" for the variable "Price in" and switch "Pay in" the currency value will be set.

Figure 4 - Settings of an agreement with a non-resident

If the details are configured correctly and the loaded courses are up-to-date *, all the data necessary for calculations will be filled in 1C documents automatically.

* Rates can be loaded in manual or auto-mode into the information register "Currency rates".

For manual loading, open the "Currencies" directory in the "Reference books / Bank and cash desk" section and click "Load currency rates".

Figure 5 - Directory "Currencies"

You can add a new currency to the directory by clicking the "Create - New" button, or select the required one from the classifier by clicking the "Create - By classifier" button.

Figure 6 - Adding currency from the classifier

For automatic loading, the settings of the scheduled task of the same name are performed.

Accounting for exchange rate differences in 1C 8.3

So, if the listed settings in the 1C program are performed correctly, then the exchange rate difference is reflected automatically:

- By date of operation, by means of the document that registers this operation. For example, through the documents “Receipt / write-off from the current account”, “Sale / receipt of goods”.

- At the end of the month by means of "Revaluation of foreign exchange funds", which is automatically launched in the "Close of the month" procedure.

Reflection of exchange rate differences in 1C 8.3

Example # 1. In terms of purchasing goods under a contract in foreign currency

In our example, under a contract with a supplier, the goods were shipped before payment. This event was recorded through the Goods Receipt document.

Figure 7 - Contract with the supplier

Figure 7 - Contract with the supplier

The rate in "Goods receipt" was filled in automatically from the information register "Currency rates".

Figure 8 - "Receipt of goods"

Figure 8 - "Receipt of goods"

Figure 9 - Transactions on "Goods receipt"

Figure 9 - Transactions on "Goods receipt"

The payment was made a few days later than the shipment and was registered in the program using the document "Write-off from the account". The currency rate in it was filled in automatically from the “Currency Rates” register, the “Amount” variable contains the value of the withdrawal amount in rubles, the “Settlement amount” variable contains the value of the withdrawal amount in foreign currency. The currency rate on the date of payment is filled in the "Settlement rate" variable.

Figure 10 - Document "Write-off from bank account"

Figure 10 - Document "Write-off from bank account"

The posting on the exchange rate difference in this case was displayed by the document "Write-off from the settlement account", since the creditors' value was recalculated at the date of settlement of the liability, i.e. on the date of payment.

The exchange rate difference is equal to 702 752.79 - 706 446.64 \u003d | -3 693.85 | \u003d 3 693.85 rubles. The resulting value coincides with the value in the exchange rate difference entry Dt 91.02 - Kt 60.31 in the document "Write-off from the current account". Thus, the negative exchange rate difference was reflected in account 91.02 “Other expenses”.

Figure 11 - Postings on the document "Write-off from the bank account"

Figure 11 - Postings on the document "Write-off from the bank account"

Example # 2. In terms of currency trading

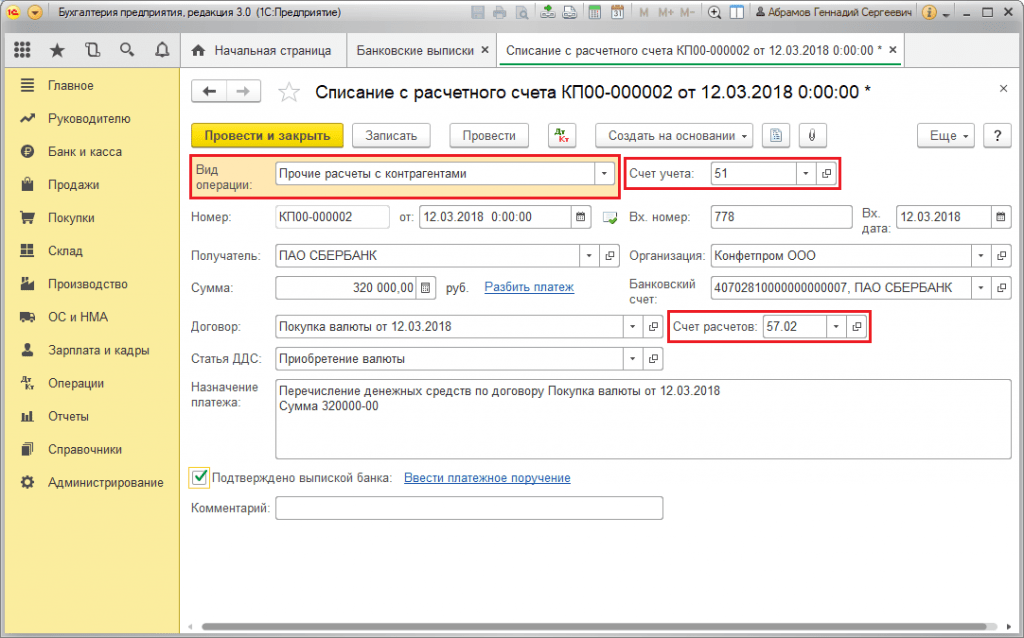

As part of the operation buying currency the transfer of DS to the bank is carried out through the document "Write-off from the settlement account" (type "Other settlements with counterparties"). The "Accounting account" variable contains account 51 "Settlement accounts", and "Settlement account" - 57.02 "Purchase of foreign currency".

Figure 12 - Transfer of funds to the bank for the purchase of currency from the document "Write-off from bank account"

Figure 12 - Transfer of funds to the bank for the purchase of currency from the document "Write-off from bank account"

Figure 13 - Transactions "Write-off from the bank account"

Figure 13 - Transactions "Write-off from the bank account"

For crediting the purchased currency to the account (respectively, foreign currency) comes from "Receipt to account" with the operational type "Acquisition of foreign currency". The line "Accounting account" contains account 52 "Currency accounts", and "Settlement account" - 57.02 "Purchase of foreign currency". "Bank rate" contains the exchange rate set by the bank for the purchase of currency. The Central Bank rate is filled in by an automatic machine in the requisite of the same name on the date of the operation. To display the difference, "Reflect the difference in the exchange rate as part of expenses" is activated.

Figure 14 - Crediting the purchased currency to the foreign currency account through the "Receipt to the bank account"

Figure 14 - Crediting the purchased currency to the foreign currency account through the "Receipt to the bank account"

The DS in the amount of 312,406.05 rubles is credited at the exchange rate of the Central Bank and is displayed by transactions Dt 52 - Kt 57.02 "Purchase of foreign currency".

Here, the occurrence of the exchange rate difference occurs as a result of the recalculation of the DS on the date of receipt, therefore it is displayed in the "Receipt to the settlement account".

The exchange rate difference is equal to 312 406.05 - 315 700.00 \u003d | -3 293.95 | \u003d 3 293.95 rubles. The resulting value coincides with the value in the exchange rate difference posting Dt 91.02 - Kt 57.02 in the document “Receipt to the current account”.

Thus, the negative exchange rate difference was reflected in account 91.02 “Other expenses”. Posting exchange rate difference in 1C:

Figure 15 - Posting on the exchange rate difference when buying currency in the document "Receipt on account"

Figure 15 - Posting on the exchange rate difference when buying currency in the document "Receipt on account"

The amount of 320,000.00 rubles transferred for the purchase of foreign currency was more than the amount spent 315,700.00. Therefore, the balance of funds in the amount of 320,000.00 - 315,700.00 \u003d 4300 rubles must be credited to the ruble account by means of the document “Receipt to the current account” with the transaction type “Other receipt”.

Operation currency sales is carried out in a similar way:

- The transfer of funds to the bank from the foreign currency account is registered in the "Write-off from the bank account" with the type "Other settlements with counterparties". The "Accounting account" variable contains account 52 "Currency accounts", "Settlement account" - 57.22 "Foreign currency sales".

- DS crediting from the sale of foreign currency to the ruble account is carried out through the "Receipt to the current account" with the operation type "Receipts from the sale of foreign currency". "Account" and "Settlement account" contain accounts 51 and 57.22, respectively.

Example No. 3. In terms of recalculation on the final day of the month

As part of the regular operation "Revaluation of foreign exchange funds", the document is automatically launched in the "Month-closing" procedure located in "Operations / Period-closing" or in "Operations / Period-closing / Regular operations".

Figure 16 - Procedure "Close of the month"

Figure 16 - Procedure "Close of the month"

When performing the routine operation "Revaluation of foreign exchange funds", the value of the balances is converted into rubles for all accounts with the sign of currency accounting at the rate of the Central Bank of the Russian Federation in the "Currencies" directory. In case of revaluation of foreign currency funds, the balance in foreign currency shall be considered unchanged.

Figure 17 - Transactions of revaluation of foreign exchange funds

Figure 17 - Transactions of revaluation of foreign exchange funds

The balances in the regulated accounting currency (rubles) are calculated at the rate indicated in the Currencies directory at the time of the revaluation, therefore, before the operation, you should make sure that the current exchange rates of the currencies used are set on the required date of the reporting period (the final day of the month).

Purchase of foreign currency in 1C: Accounting 8.3, revision 3.0

2016-12-13T12: 24: 36 + 00: 00In this lesson, we will look at how to purchase currency in 1C: Accounting 8.3, revision 3.0.

In order not to miss the release of new lessons - to the mailing list.

I remind you that this is a lesson, so you can safely repeat my actions in your database (preferably a copy or a training one).

So let's get started

The organization has the right to buy currency on the domestic market of the Russian Federation only through authorized banks and only for the following purposes:

- payment to a foreign supplier for goods, works or services (import)

- payment of customs duties in foreign currency

- payment of the employee's expenses for a business trip abroad

- payment of a foreign currency loan

To do this, the organization sends an order to the bank to buy currency.

The organization must indicate at its disposal:

- what is the purpose of the currency

- documents that formalize the transaction, for the payment of which the currency is bought (for example, a contract with a foreign supplier, a loan agreement, etc.)

Working example

We need to buy $ 100 to pay the foreign supplier.

On January 1, 2016, we sent an order to the bank (in which we have two accounts - in rubles and in foreign currency) to purchase 100 US dollars at a rate not exceeding 75 rubles per dollar.

On the same day, the bank debits 7,500 rubles ($ 100 * 75 rubles) from our ruble account:

At the same time, in accounting, we reflect the purchase of currency in rubles at the exchange rate of the Central Bank of the Russian Federation on January 2 (it was equal to 72.9299 rubles per dollar):

The bank's commission for the purchase of currency was 100 rubles:

It would seem that everything? Not.

Firstly, we must reflect in the accounting the difference between the rate of the Central Bank of the Russian Federation (72.9299) and the rate at which our bank acquired currency for us.

If the purchase rate of our bank turned out to be lower than the rate of the central bank, then we have a non-operating income in the amount of the difference in rates multiplied by the amount of purchased currency.

If the purchase rate of our bank turned out to be higher than the rate of the central bank, then we have a non-operating expense in the amount of the difference in rates multiplied by the amount of purchased currency.

In our case, the bank's buying rate (73 rubles) is higher than the rate of the Central Bank of the Russian Federation (72.9299), so we reflect the other expense in the amount of $ 100 * (73 - 72.9299) \u003d 7 rubles and 1 kopeck:

Secondly, the money remaining after the purchase of currency (minus the difference between the rates) will be returned by the bank to our ruble account 7,500 - 7,292.99 - 7.01 \u003d 200 rubles:

Now we will issue all these operations in 1C: Accounting 8.3, revision 3.0.

Loading currency rates

We issue a write-off from a ruble account for the purchase of currency

We go to the section "Bank and cash desk" item "Bank statements":

We create a document for debiting 7,500 rubles from our ruble account to the bank for the purchase of currency:

We fill out the statement:

We carry out the document:

We make out the receipt of currency to a currency account

In the same journal "Banking statements" we create a receipt for our current foreign currency account of 100 US dollars:

We fill out the statement:

We carry out the document:

We issue a refund of unspent funds for the purchase of currency

In the same journal "Bank statements" we create a document of receipt of the funds remaining on account 57 (200 rubles).

At the present time, no one can be surprised by the presence of foreign exchange transactions in the daily activities of the organization. Export and import open up new opportunities for the successful development of the enterprise, and the accountant has to come to terms with the emergence of a separate branch of accounting - working with currency. In the program "1C: Enterprise Accounting 8" edition 3.0, all the functionality necessary to reflect currency transactions is presented, and in this article I would like to focus on buying currency and its correct accounting in this program.

First of all, I would like to draw your attention to the fact that an organization has the right to purchase currency only through an authorized bank, and there is a separate account 52 for making payments in foreign currency in accounting. At the same time, to make payments, you need to have 2 current accounts in the bank: and currency.

As always, for correct work on this section of accounting in the program, you need to make some settings. Let's start by setting up functionality:

The following form opens:

This form allows you to configure a wide range of different functions, but now let's look at the "Calculations" tab.In order for currency transactions to become possible in accounting, the following flags must be set:

Since transactions with currency must fall into the form No. 4 of the regulated financial statements, it is necessary that this analytics be kept in the accounting.

To do this, we will carry out the following setting in the program's chart of accounts:

After opening the form, click on the "Setting up a chart of accounts" hyperlink:

In the settings form, we will also follow the link:

In the window that opens, pay attention to the flag in the variable "By items of cash flow":

If the flag is not set, it must be set. This setting allows you to keep records in the context of analytics "Cash flow items". After setting the flag, this subconto will appear on all cash accounts:

I also want to note that if an organization in its accounting assumes the use of account 57 "Transfers in transit" when reflecting banking operations, then this setting must also be set. In general, this account is recommended to be used if there is a possibility that the order to the bank to buy foreign currency (and hence the deduction of the ruble amount from the current account) and the receipt of the amount to the foreign currency account by dates may not coincide. If transactions take place within one day, then this account may not be used.

This setting is located in the accounting policy settings. It can be found in the program as follows:

You need to set the flag:

At this point, we will finish with the settings of the program for accounting for currency and start directly reflecting currency transactions in 1C.

The first thing that needs to be done is to send an order to the bank to buy currency (indicating the purpose of buying currency, documents confirming the need to buy currency, the amount of currency and the maximum rate for the purchase). This order is a printed form, which is developed by the bank independently. To withdraw amounts from the current account, a payment order is generated. In the program 1C: Enterprise Accounting 8, this can be done on the "Bank and Cashier" tab.

The bank debits the amount required for the purchase from the ruble account. Let's execute this operation in the program:

In the document "Write-off from the current account", select the type of operation "Other settlements with counterparties":

We also fill out an agreement with the bank, which we entrust the purchase of currency. The contract must be of the "Other" type:

Next, we indicate the item of cash flow - it is necessary to indicate "Purchase of foreign currency (write-off)". If your account uses account 57, then in the "Settlement account" requisite you must indicate "57.02", if accounting without it, then account "76.09":

In the requisite "Bank account" we indicate the ruble account, since the debiting is carried out from the organization's ruble account.

After execution, the document generates the following account movements:

After debiting the ruble amount from the current account, the bank executes our order and purchases currency. Since in accounting, the storage of foreign currency is carried out in rubles (for data accuracy), when currency amounts and other operations with currency are received on the account, the amount is converted into the ruble equivalent. In order for the recalculation to be made on the basis of the current exchange rate, it is necessary to promptly update the data in the "Currency rates" reference book. The program has the ability, if you have an Internet connection, to automatically download the exchange rate of the Central Bank of Russia:

To register the fact of buying currency, the document "Receipt to the current account" is generated.

We fill in the document with the necessary data:

1. Type of operation - “Purchase of foreign currency”;

2. In the requisite "Amount" we indicate - the amount of purchased currency;

3. In the requisite "Bank account" - the organization's foreign currency account. Please note that the contract must indicate the currency (in our case "USD").

In the requisite "Bank rate", you must indicate the rate at which the bank bought the currency on our instructions. Accordingly, the “Amount in rubles” variable will reflect the amount spent by the bank. In the requisite "Central Bank rate" - the rate that is relevant on the date of the transaction. The flag "Reflect the difference in the rate in the composition of expenses" determines the crediting of the lost difference between the rate of the Central Bank and the rate of our bank:

After being carried out, the document forms the following movements:

In our case, the second posting transfers the currency amount to the organization's foreign currency account, the third posting writes off the incurred losses due to the difference in the rate of the Central Bank with the rate of the bank that purchased the currency for us.

I will also dwell on the first posting in more detail. It means that there was a certain currency amount on the organization's foreign currency account, which was also revalued, the difference in exchange rates was reflected (in this case, the currency fell in price and the organization suffered losses). I also want to note that the revaluation of funds and liabilities in foreign currency is carried out on the day when movements are made on the foreign currency account and at the end of the month, regardless of the presence / absence of transactions on it. For revaluation at the end of the month, a special routine operation "Revaluation of foreign exchange funds" is intended, which is performed as part of the complex of operations "Close of the month":

Since the bank was transferred the amount of 75,000 rubles, and the purchased currency was in the amount of 73,750 rubles, then we need to return the difference to the ruble account.

We will also use the document "Receipt to the current account":

After filling out, we will post the document, the following transactions are formed:

This completes the currency purchase operations. You can check the state of the accounts using the "Balance sheet" report.

but you don’t know how to correctly arrange the purchase and sale of currency in the 1C Accounting program (version 3.0) - in this case, this article will help you.

This material clearly shows how to record transactions of buying and selling currency in 1C in accordance with Russian legislation.

Accounting for currency transactions

First, we will briefly and briefly understand the procedure for accounting registration of the operations of interest to us.

According to Article 14 of Federal Law No. 173-FZ "On Currency Regulation and Currency Control", organizations can open, without restrictions, special currency accounts in authorized banks for conducting transactions in foreign currency. To account for such a currency in the chart of accounts there is a special account 52 "Currency accounts", the debit of which reflects its receipt (including purchase), and the credit - write-off (including sale).

Accounting for currency is subject to PBU 3/2006 "Accounting for assets and liabilities, the value of which is denominated in foreign currency". The Regulation establishes the need to recalculate the value of the relevant assets into rubles at the official exchange rate. The recalculation should be carried out on the date of the foreign exchange transaction, as well as on the reporting date (for the purposes of preparing financial statements). In this case, there may be:

- Positive exchange rate differences: for accounting - other income (clause 7 of PBU 9/99); for tax accounting - non-operating income (article 250 of the Tax Code of the Russian Federation);

- Negative exchange rate differences: for accounting - other expenses (paragraph 11 of PBU 10/99); for tax accounting - non-operating expenses (article 265 of the Tax Code of the Russian Federation).

It should also be noted that when selling currency, ruble receipts from this operation are qualified as other income (account 91.1), and the corresponding disposal - as other expenses (account 91.2).

Presetting the program 1C 8.3 Accounting

If the transfer of funds between the currency and settlement bank accounts does not take place within one day, then you should use the intermediate account of the chart of accounts 57 "Transfers in transit", otherwise account 76.09 "Other settlements with different debtors and creditors" can be used.

In our example, we will follow the first path, so we need to check if the account 57 is connected to the organization in the 1C Accounting 8.3 program. To do this, open the list of accounting policies of organizations. Section General - command group Settings - command Accounting policy:

Then we will open the current accounting policy for editing (corresponding to the required organization and period):

In addition, we will make sure that the possibility of maintaining is established in the Accounting Department of 1C 8.3. For our release of the 1C Accounting 8.3 configuration, the corresponding flag "Calculations in currency and USD" located on the Calculations tab. It is possible that in your version of the configuration the setting may be on another tab, it should be found in the form "Program functionality":

You can open the form as follows: section Main - command group Settings - command Functionality:

Set in the active state the flag "Calculations in currency and USD" makes available to the user in the chart of accounts foreign currency accounts, and also allows you to select the foreign currency of the calculation in the created contracts with counterparties:

Since in the example we will work with foreign currency and convert to the ruble equivalent, we need to store and periodically update the list of currency rates for different dates in 1C 8.3. The 1C Accounting program allows you to automatically download the required exchange rates for the required period. This is done as follows:

- Let's open the list of currencies. References section - Buy and Sell command group - Currency command:

- On the form that opens, click the Download Currency Rates button, then in the window that appears, select the currency and set the download period, then click Download:

Buying currency in 1C 8.3 using the example of postings

Consider the following example of buying currency in 1C 8.3:

10.06.2016 the organization buys through an authorized credit institution EUR 10,000.00 at the market price of currency purchase of RUB 74.00 / EUR. The official euro exchange rate established by the Central Bank of Russia on the date (June 11, 2016 - the day of receipt of money on the bank foreign currency account) of the transaction is 73.1909 rubles / euro.

First of all, we will issue in 1C Enterprise Accounting 3.0 the transfer of funds from the current account for the purchase of foreign currency. Since the final transfer will take place not on the same day (06/10/2016), but on the next day (06/11/2016), we will use the transit account 57 “Transfers in transit”, the result will be the following:

- Debit 57.02 - Credit 51.

So, for this we will create a document Write-off from the current account. Section Bank and cash desk - group of commands Bank - command Bank statements. In the form that opens, press the Write-off command:

To begin with, you should select the appropriate type of operation - in our case it will be "Other settlements with counterparties". Further, in addition to the main standard details, account 57.02 “Purchase of foreign currency” is indicated in the field of the tabular section of the Settlement account, and the corresponding analytics is also filled in in the form of an agreement with a counterparty and an item of cash flow. Please note that the type of agreement must be in the value "Other", and in the "Price in" variable in the Calculations section, rubles are indicated.

At the output, we get the expected wiring:

According to the terms of the problem, the purchased currency is credited to the foreign currency account on the next day, 06/11/2016:

- Debit 52 - Credit 57.02: reflected the purchased foreign currency (EUR 10,000.00) valued in rubles at the exchange rate of the Bank of Russia (as of 06/11/2016) (EUR 10,000.00 * 73,1909 RUB / EUR + 731,909.00 rub.).

- Debit 91.02 - Credit 57.02: the exchange rate difference (between the contractual selling rate and the official rate) is reflected in other expenses.

Now you need to enter the document Receipt to the current account. Section Bank and cash desk - group of commands Bank - command Bank statements. In the form that opens, click the Receive command.

Here we act in a similar way to the procedure for filling out the previous document 1C Accounting 3.0. To begin with, you should select the appropriate type of operation - in our case, "Purchase of foreign currency" Further, in addition to the main standard details, the tabular section indicates the settlement account - 57.02, and the corresponding analytics is also filled in in the form of an agreement and an item of cash flow.

Note a number of the following salient points:

- In the requisite Accounting account, select account 52 (it will appear in the debit of the transaction);

- In the Bank account requisite, select a specially established foreign currency bank account, in turn, the Account Currency requisite of which is set to EUR (ie Euro);

- In the Bank rate field of the tabular section, indicate the currency purchase rate from the bank under the agreement;

- By checking the box “Reflect the difference in the exchange rate in the composition of expenses”, we achieve the calculation and recognition of the exchange rate difference as other expenses (income). The above checkbox can be removed, then you must independently take into account the exchange rate difference by making a manual posting through the Operation document. Section Operations - group of commands Accounting - command Operations entered manually;

- If necessary, you can independently indicate the rate of the Central Bank of the Russian Federation. By default, it is automatically "picked up" from previously loaded courses in accordance with the date of the document:

At the exit, we get the expected posting, reflecting the transfer of funds to:

To check the movements on accounts 52 and 57.02 "Acquisition of foreign currency", we will generate balance sheets for them. Section Reports - group of commands Standard reports - command Balance sheet by account.

As you can see, the turnovers and account balances correspond to the conducted business transactions:

Selling currency in 1C 8.3 for example

We continue the example, where we will consider step by step how to sell currency in 1C 8.3:

06/15/2016 the organization decides to sell (at the exchange rate of 73 rubles / euro) 3,000.00 euros in its foreign currency account, about which a corresponding order was given to the bank. Cash from the sale of foreign currency was transferred to the settlement account of the organization on June 16, 2016.

At the first stage, we write off funds from a foreign currency account to sell foreign currency. Since crediting to a bank current account takes place the next day, we use account 57:

- Debit 57.22 - Credit 52.

Create a document Write-off from the current account:

- Operation type - Other settlements with counterparties;

- Accounting account - 52, that is, we indicate the currency account from which foreign currency is debited for sale;

- The field Agreement of the tabular part of the document - create in 1C Accounting and enter data on the agreement with the bank, according to which the sale of foreign currency is carried out (in the “Price in” variable in the “Calculations” section, in our case, we indicate EURO, ie Euro);

- The field of the Settlement account of the tabular section of the document is 57.22, that is, we indicate a special transit account Sale of foreign currency:

By clicking the Show transactions and other document movements button (see the figure above), you can view transactions created from the sale of currency in 1C 8.3:

Since the euro exchange rate has increased compared to the moment of the last ruble valuation of foreign currency ((74.3174 - 73.1909) * 10,000.00), as a result of the recalculation, we obtain a positive exchange rate difference, recognized as other income and accounted for on account 91.01 in the amount RUB 11,265.00

At the second stage, we register the proceeds from the sale of foreign currency received on the next day to the current bank account, for which the document Receipt to the current account with the transaction type Receipt from the sale of foreign currency is used in 1C Accounting 3.0:

The nuances of filling:

- The field Calculation rate of the tabular section of the document - indicates the rate at which the bank acquired foreign currency from the organization;

- The field of the Central Bank of the Russian Federation of the tabular section of the document is filled in automatically based on the previously loaded exchange rates (see above).

After filling out and posting the document, let's move on to viewing the transactions made by it:

As you can see

- The first entry was registered, as a result of which, in our case, a negative exchange rate difference in the amount of 1,119.90 rubles was formed, attributed from the credit of account 57.22 to other expenses. (3,000.00 * (73.9441 - 74.3174)).

- The next entry in the order registered income from the sale of foreign currency at the bank's contractual rate in the amount of 219,000.00 (3,000.00 * 73).

- Then there is a posting reflecting the write-off of the sold currency to other expenses (D-t 91.02) in the amount of 221,832.30 (3,000.00 * 73.9441; at the official rate of the Bank of Russia on the date of the currency transaction).

- Further it is registered in accordance with paragraphs. 6 p. 1 of Art. 265 of the Tax Code of the Russian Federation, the tax constant difference resulting from the deviation of the actual selling rate of foreign currency from the official one. As a result, all three registered constant differences "offset" each other, that is, they give zero balance.

- The last two transactions register non-operating expenses and income not accounted for for tax purposes on off-balance sheet accounts - this is auxiliary information that accompanies the routine operations of the month-end closing.

To check the movements on accounts 52 and 57.22 "Foreign currency sales", we will generate balance sheets for them:

I wrote how to buy currency at the bank. Further, for any accountant, the question arises of how to carry out these operations correctly. Further I will tell you how to register the purchase and sale of currency in 1C Enterprise 8.2.

First you need to create two Contracts for the counterparty - the bank.

Let's call the first Agreement "Buying Dollars". Type of contract: "Other". Settlement currency:"Rubles"

The second Agreement will be called "Dollars Sale" Type of contract: "Other". Settlement currency: "USD"

Let's start by buying currency.

Write-off from the current account

Transaction type: Other write-off.

Next Fill in the amount and debit account 57.02, counterparty - bank, Agreement - "buy dollars"

The next step is to select the receipt to the current account. Receipt type - "Purchase of foreign currency"

It is important to set the account here: 52 !!!

Choose a bank account in dollars !!!

And then put down the amount in currency and the rate, or the amount in currency and dollars. All this information is contained in the statement.

Another important nuance, you must have uploaded exchange rates for the dates of transactions. This is done either manually, or you can configure the autoloading of currency rates. Here I have already described how to make life easier for myself:

The second question is the registration of the sale of currency.

The principle is the same here. But the Agreement "Sale of dollars" is used (settlements under this Agreement in foreign currency!)

1. Write-off from the current account - other.

Put accounting account 52, bank account in foreign currency. Account 57.22, counterparty - bank, Agreement - "Sale of dollars".

2. Receipt to the current account - receipts from the sale of foreign currency.

Accounting account - 51, bank account in rubles. Counterparty - Bank, Agreement - "Buying Dollars"

Then fill in according to the statement, the amount in currency, the rate, check the amount in rubles.

In this case, at the end of the documents, be sure to check the balance of account 57.02 and account 57.22. It should be zero. If not, look for an error. Check both documents step by step. Major mistakes:

- different dates of debiting and crediting documents

- the account is incorrectly indicated in the upper left corner

- the document of enrollment was not selected correctly

And all the same for all other currencies, respectively.